Tian Chang Group is a HK-listed Plastics Manufacturing company. In their own words: “We are a well-established provider of integrated plastic solutions in the PRC. For over 17 years, we have specialised in mould design and fabrication services as well as plastic component design and manufacturing services. In recent years, we have also expanded our operations to the manufacturing of e-cigarette products as an OEM.” Although the company has a relatively long history, it only got listed in March 2018. Currently the stock price is down around 25% from the IPO level. Underlying business performance shows a totally different picture though.

Description of the business

Integrated plastics: Tian Chang is fabricating highly precise moulds and uses those to produce plastic parts mostly for electronic goods and office furniture. The plastic injection moulding business is a highly competitive business with China having tens of thousands of competitors. There are differences in capabilities though. A few big customers are responsible for the lion’s share of the sales (Panasonic, Brother, …). The clients seem to be an indication of their high quality claim.

E-cigarettes: They are an OEM for the E-cigarette brand called “Blu” from Fontem which is a subsidiary of Imperial Brands (a big UK tobacco company). They operate under a long term agreement with them. Part of the agreement is that they can only produce for Fontem, volumes and prices are not fixed. They are a price taker. Recently they expanded the scope of products and are trying to in-house manufacture more of the components they previously bought from other suppliers (eg. the smoke liquid bottles and the PCBA). In the IPO prospectus, they were claiming to be a supplier for around 25% of the E-cigarette COGS of Fontem. This industry also looks like a highly competitive business, although from the brands point of view, there might be some incentives to not focus solely on cost but also on quality and trustworthiness.

Both segments are vulnerable to rising raw material and labor costs. Tian Chang is upgrading a lot of their equipment in order to get more automated. This will improve quality and bring labor costs down.

Growth

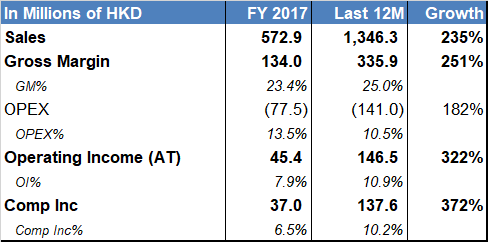

FY2019 earnings are not available yet but let’s take 12M Trailing numbers to compare with FY2017.

The growth of Sales and Gross Profits have been concentrated in the E-cigarette segment. As a reference, check the following graphs (ignore the S1 2017 numbers, S2 2017 was not readily available).

Tian Chang does not disclose much detail into the underlying developments of their revenues. So I can’t really figure out if S2 2018 sales for the integrated plastics department will be repeatable or not. One thing for sure is that they are adding a lot of sales in the E-cigarettes.

Profitability

Return on Net Operating Assets has skyrocketed with increasing sales.

If we break it down we can see that both the Profit Margin and the Asset Turnover improved over time. Let’s take a look at the Profit Margin first.

As you can see on the graph, the Profit margin improvement stems from a steady gross profit margin coupled with an operating leverage effect. The operating costs are spread over a bigger Gross Profit.

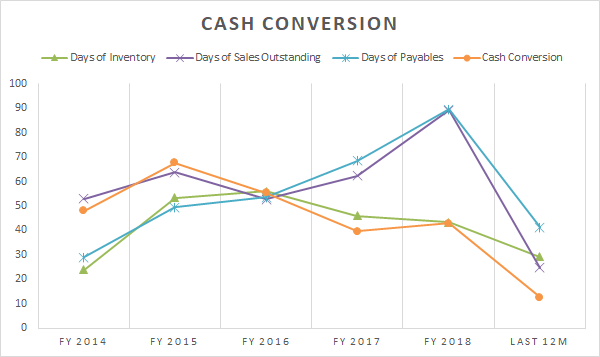

If we look at the Asset Turnover, we can see that the capital has been used more efficiently. The biggest component in the Asset turnover is the PP&E. PP&E net of depreciation has only increased slightly while ramping up sales. Working capital is very limited as you can see in the Cash Conversion graph.

Payments for orders on the E-cigarette segment are generally settled within 10 days. This means this very fast cash conversion as long as the E-cigarette segment dominates.

Outlook

For the integrated plastics segment I would estimate that they will continue to grow slowly as more competitors are driven out of the market. Rising labour costs in China, will make sure that the small producers, that can not invest in automation, will be driven out of the market. The end market will keep on growing slowly.

Despite all the negativity lately, I do expect the E-cigarette market to expand quite fast mainly through substitution from classical tobacco users. There are health benefits to switching. This growing total market, does not necessarily mean that Tian Chang will be a big beneficiary of this trend. First of all, Blu could underperform. Eg. In the US, Blu has a very strong competitor in Juul. Statistics from the IPO prospectus said the following: “Fontem is one of the leading e-cigarette brand owners and “blu” was the third largest e-cigarette brand worldwide with 4.2% global market share in 2016 in terms of sales value,according to the Frost & Sullivan Report.”

I have no access to more up to date research reports but it would seem that Blu is losing some market share. However the market is growing fast and seems like Tian Chang is gaining market share between the suppliers to Blu.

Most of this is guesswork because Tian Chang does not provide much information. We do have two good information points though.

- Sales in the E-cigarettes segment has grown a lot.

- In October 2019, they signed a construction agreement for a new factory with an accompanying dormitory. They plan to increase capacity by around 55% in the E-cigarettes and 20% in the integrated plastics.

Risks

- Corporate governance: In June 2019, the chairman and controlling shareholder sold 14.8% of the company to a former executive director for 48 HKDcents. This price was very low compared to intrinsic value. He still holds 60.2% now. The concern is mainly about why he would sell at such a very low price. I suspect this was kind of a pre agreed trade. Before the company was listed, this former executive director also held shares as a trustee for the chairman.

- Corporate governance: The three executive directors had a salary of around 18.5M HKD. I think this is on the high side for a company this size. On the other hand they seem to be executing well.

- The Current ratio is below 1. This might be a feature and not a bug. Working capital requirements are very low. Cash conversion is very fast. They have used a lot of cash to pay off debt. Interest paying obligations net of cash have gone down from 222M to around 55M HKD. Also the current portion of the debt is probably classified as current because it is payable on demand. This does not mean it needs to be repaid immediately. I suspect their financial situation will improve rapidly and markedly.

- Commodity business: In both segments there are thousands of potential competitors. The only thing Tian Chang might have as a competitive advantage is some higher (perception) of quality, trust, reliability and long relationships with their customers. They are especially vulnerable since their customers account for a very large percentage of the sales. Gross profit margins have been relatively steady which indicates some of the above mentioned competitive advantages might be present. Especially the E-cigarette business might be vulnerable if there is a change at Fontem. Tian Chang does not seem to have any control over the price so this is concerning.

Valuation

- Base Case: The company has been performing extremely well, but since it has a relatively short track record I think a good margin of safety is in order. We should not assume that everything goes well and according to plan in the base case. Sales growth is 5% for the next 5 years and settles at 2%. Profit margins go down to 8% because of their reliance on a limited number of customers and keen competition. In this case, the intrinsic value would be around 1.22 HKD, which implies an IRR of around 30%.

- Downside Case: For the downside case, I assumed reverting back to the situation before the ramp up. Roughly 600M in sales and 8% profit margin. I have also omitted potential cash inflows from scaling down. The intrinsic value would be 0.43 HKD. This implies an IRR of around 13%. This downside scenario certainly validates the fact that the margin of safety in this investment is big.

- Bullish case: I have added a big ramp-up in sales in T+2. This was calculated based on the capacity increase they announced in October 2019. Roughly 55% for Ecigs and 20% for integrated plastics. I model a profit margin of 12.5% based on the operating leverage we have seen during the last ramp up. (I would estimate I am probably too conservative.) The sales increase in T+2 is accompanied by a cash outflow for CAPEX of 285M. All this results in an intrinsic value of 2.26 HKD.

Hi This is Stephen, I noticed that you are a follower of Dream International too. I have been following this company for 5 years and prepared a long writeup on this idea too. My email is stephenpeng1207@gmail.com. Let’s see whether you are interested to meetup for a coffee and have a chat in Hong Kong.

http://www.valueasia.org/businesses/dream-international-limited-sehk1126-part-1/